How First In, First Out (FIFO) Works The FIFO method is used for cost flow assumption purposes. In manufacturing, as items progress to later development stages and as finished inventory items are sold, the associated costs with that product must be recognized as an expense.

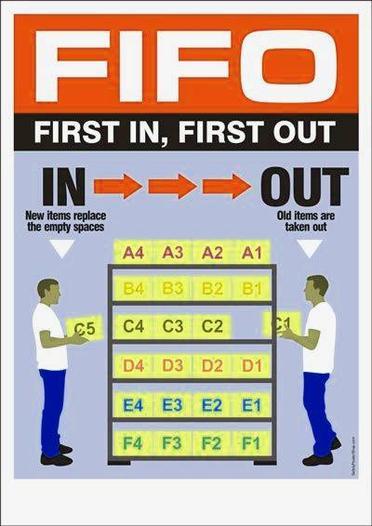

First-In, First-Out (FIFO) is one of the methods commonly used to estimate the value of inventory on hand at the end of an accounting period and the cost of goods sold during the period. This method assumes that inventory purchased or manufactured first is sold first and newer inventory remains unsold.

First-In, First-Out Inventory Method First-In, First-Out (FIFO) is one of the methods commonly used to estimate the value of inventory on hand at the end of an accounting period and the cost of goods sold during the period. This method assumes that inventory purchased or manufactured first is sold first and newer inventory remains unsold.