Mesopotamia Economy: First Contracts and Banking Systems

Ancient Mesopotamia had the worlds first known written contracts and banking-like systems. Temples served as banks, storing grain and issuing loans.

World economy charts, business frameworks and diagrams

Ancient Mesopotamia had the worlds first known written contracts and banking-like systems. Temples served as banks, storing grain and issuing loans.

The first ATM, installed in London in 1967 by Barclays, changed banking forever, allowing 24/7 cash access and setting the stage for global automated banking.

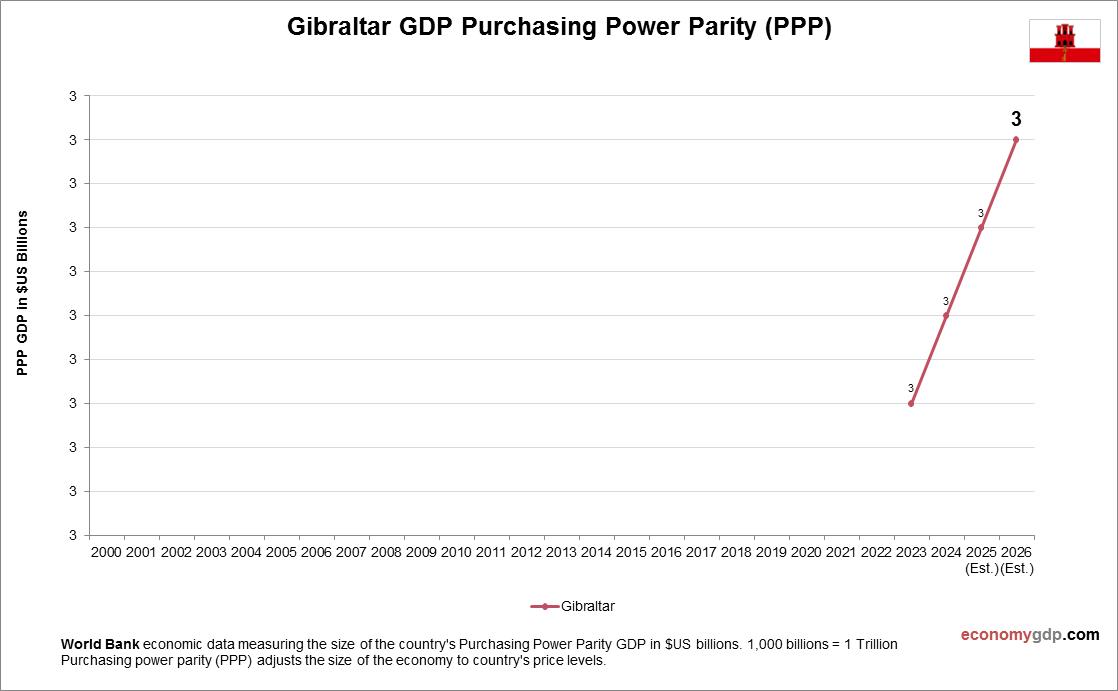

Gibraltars PPP GDP was approximately $3.7 billion in 2023. Financial services, gaming, and tourism dominate, with GDP per capita (PPP) around $92,000. Its tax haven status drives growth, but Brexit and regulatory scrutiny pose risks. Diversification into tech is emerging. View diagram Gibraltar GDP PPP

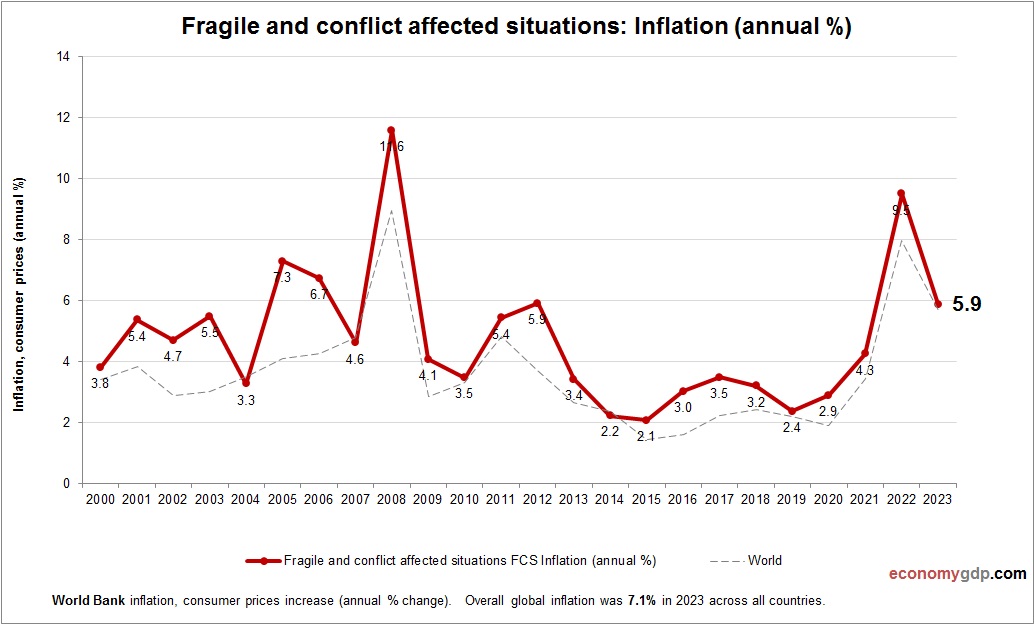

This graph shows Fragile and conflict affected situations Inflation. The consumer price statistics are compiled by World Bank. Based on the latest economic data provided for Fragile and conflict affected situations. Inflation in fragile and conflict-affected situations is typically caused View diagram Fragile and conflict affected situations Inflation

Barbados GDP (PPP) is projected at $6.7 billion in 2025. Tourism is the economic cornerstone, contributing nearly 40% of GDP, with luxury resorts and beaches drawing visitors. The PPP adjustment accounts for a high cost of living, moderating GDP figures. View diagram Barbados GDP Purchasing Power Parity

Yemen exported coffee in the 15th century, sparking global trade and coffeehouses across Europe, creating one of the first international commodities.

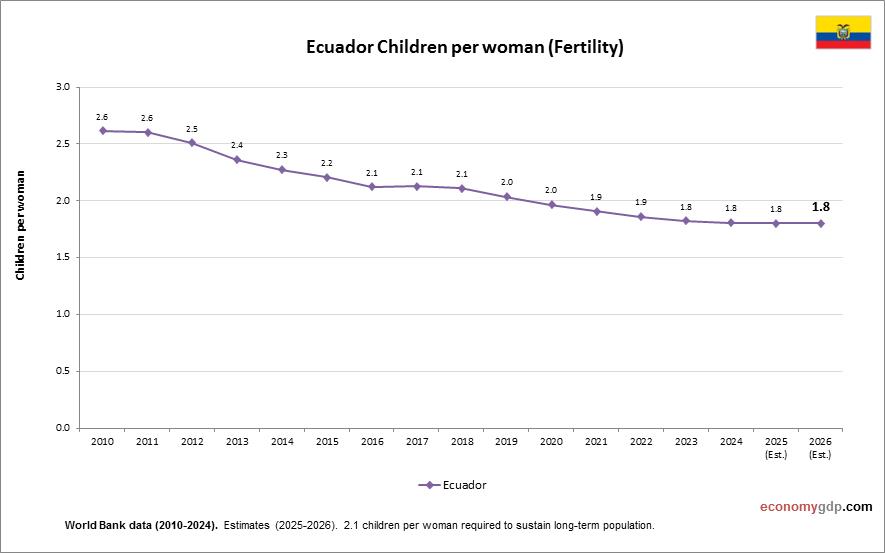

Chart above demonstrates Ecuador Children Per woman. The fertility rate statistics are compiled by World Bank. Based on the latest demographics info provided for Ecuador. Ecuadorian women have approximately two children, influenced by urbanization and expanding healthcare services. Ecuador Children View diagram Ecuador Children Per woman

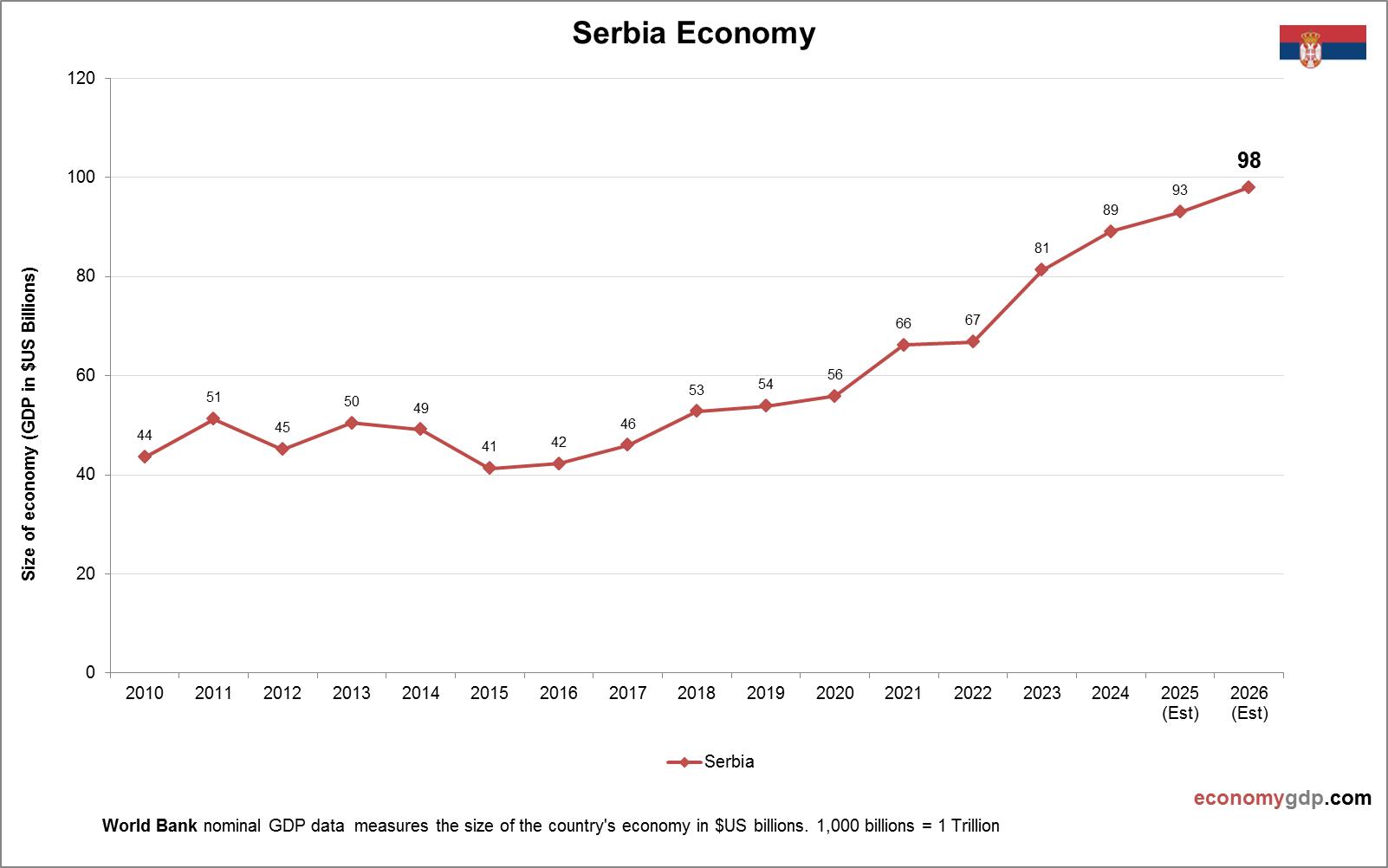

Serbia's economy features agriculture, with fruits and grains. Manufacturing in autos and food processing grows. Belgrade's IT sector emerges. EU candidacy attracts investment. Challenges include corruption and emigration. Efforts target energy. Serbia's Balkan position aids trade. Reforms promise integration. World View diagram Serbia Economy

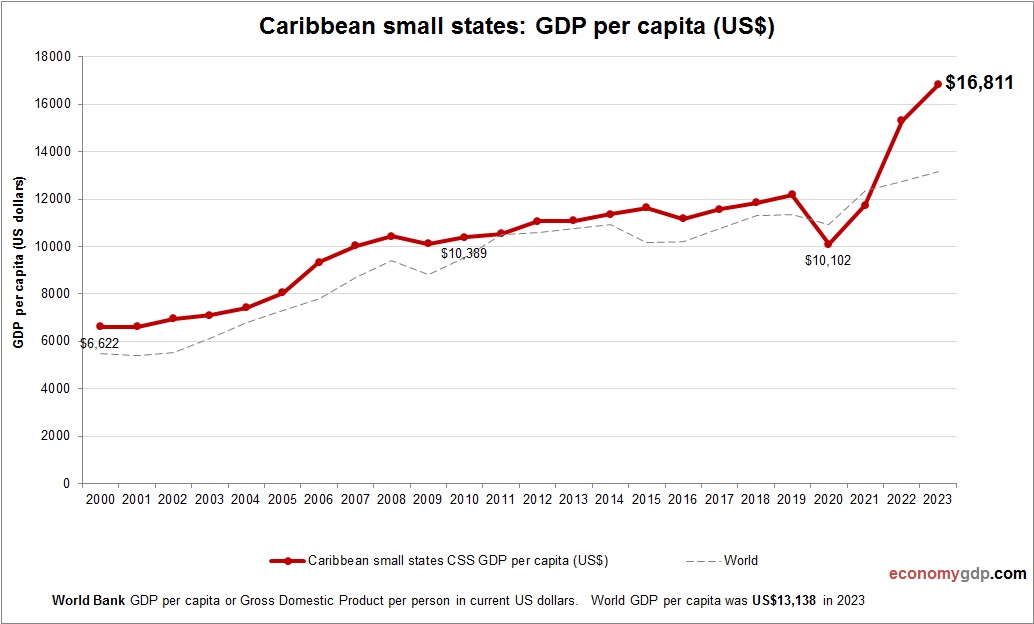

This chart demonstrates Caribbean small states GDP per capita. The gross domestic product statistics are compiled by World Bank. Based on the latest available information for Caribbean small states. Caribbean small states exhibit a wide range of GDP per capita View diagram Caribbean small states GDP per capita

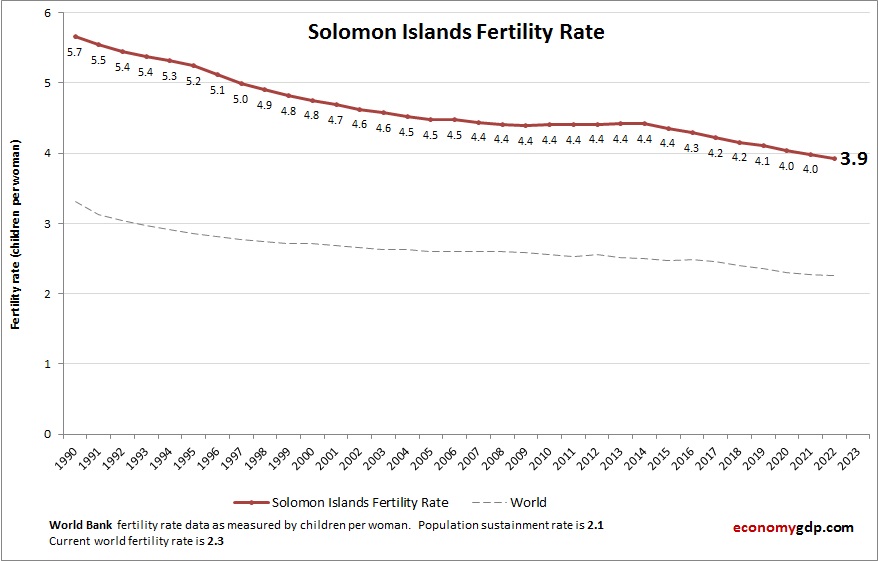

This diagram presents Solomon Islands Fertility Rate. This is according to World Bank birth stats by country. Based on the latest available information for Solomon Islands. The Solomon Islands maintain a relatively high fertility rate, influenced by traditional cultural norms View diagram Solomon Islands Fertility Rate